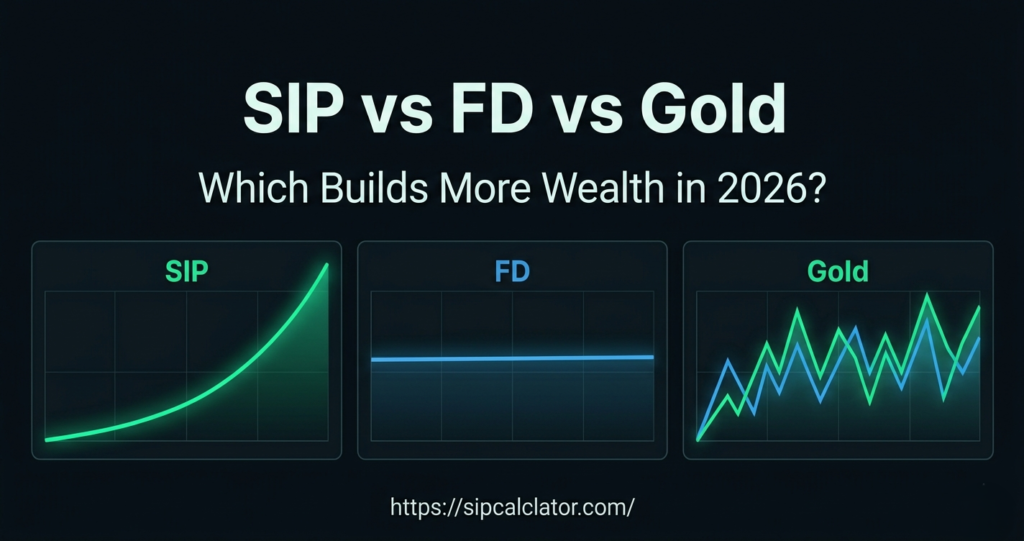

Rupee Cost Averaging

When markets fall, your fixed SIP amount buys more mutual fund units. When markets rise, you buy fewer. Over time, this averages out your cost per unit — protecting you from investing a large amount at a market peak.

Power of Compounding

Returns earned on your investment begin earning their own returns. This compounding effect accelerates dramatically over time — a ₹10,000/month SIP over 20 years at 12% grows to over ₹99 lakhs, with only ₹24 lakhs invested directly.

Disciplined Investing

SIPs run on auto-debit from your bank. This removes the temptation to skip investing during market downturns — which is exactly when you should be buying more. Consistency is the single biggest driver of SIP success.

High Liquidity

Unlike Fixed Deposits with lock-in periods, most SIPs (except ELSS) allow you to withdraw anytime. Your money is never trapped. You can also pause, reduce, or increase your SIP amount at any point without penalty.

Low Starting Amount

You do not need a large corpus to begin. Many reputed mutual funds accept SIPs starting at ₹100–₹500 per month. This makes SIP the most accessible wealth-building tool available to salaried individuals and young investors.

Diversification Built In

When you SIP into a mutual fund, your money is spread across dozens or hundreds of companies. This diversification means a single company's bad performance has minimal impact on your overall portfolio — unlike investing in individual stocks.

SIP Calculator

Fixed monthly SIP returns

Step Up SIP Calculator

You are here

Lumpsum Calculator

One-time investment returns

SWP Calculator

Systematic withdrawal plan